Reading time:

Why do companies release earnings reports?

Discover how earnings reports impact investors, stock prices, and company credibility. Learn what’s included, why they matter, and how to read them like a pro.

Article written by

Jared

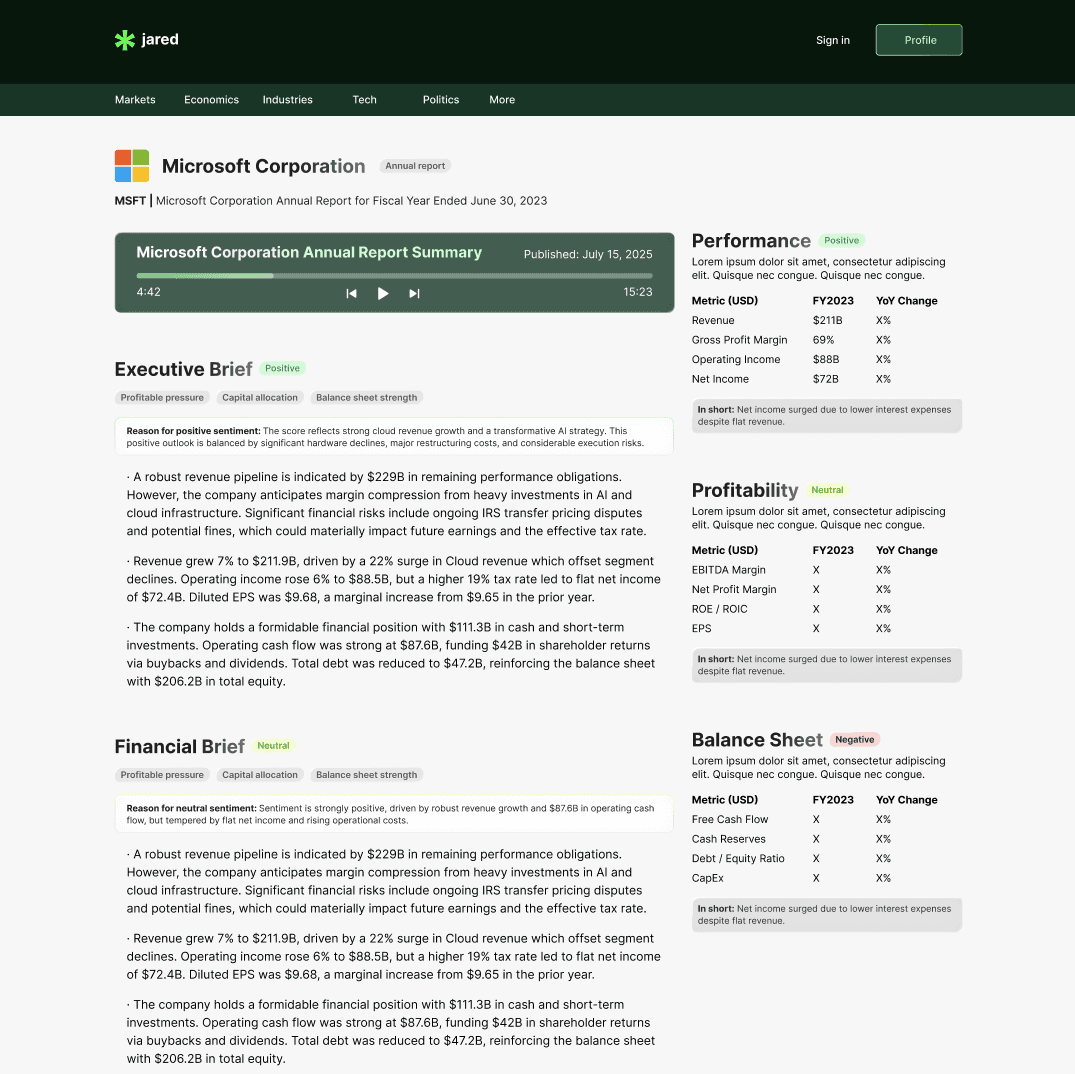

Companies regularly publish earnings reports as a structured way to disclose financial performance to investors, regulators, and the public. These documents—typically released quarterly and annually—summarize revenue, expenses, profits, cash flow, and other financial metrics, while often including management commentary on results and future expectations. Beyond fulfilling regulatory obligations, earnings reports shape investor confidence, influence stock prices, and even affect customer and partner perceptions.

Regulatory compliance and the legal baseline

Public companies operate under legal requirements to disclose material financial information on a regular basis. In the United States, the Securities and Exchange Commission (SEC) mandates periodic filings such as Form 10-Q for quarterly reports and Form 10-K for annual reports. These filings create a consistent, auditable record of a company’s financial health and reduce information asymmetry between insiders and outside investors.

Regulatory frameworks are designed to protect investors and promote market integrity. Timely and accurate disclosures allow analysts, institutional investors, and retail shareholders to compare companies on a common set of metrics and to spot red flags—such as declining margins, rising debt, or deteriorating cash flow—that could signal financial distress.

Beyond periodic filings, companies must also meet ongoing obligations around material event reporting (for example, Form 8-K in the U.S.), internal controls over financial reporting, and auditor attestation. Enforcement mechanisms—ranging from fines and disgorgement to injunctions and criminal referrals—reinforce the credibility of disclosed information and incentivize rigorous internal governance. When disclosures are later found to be materially inaccurate, restatements and enforcement actions not only harm market confidence but can trigger derivative litigation, insurance claims, and reputational damage that compound the financial fallout.

Internationally, disclosure regimes vary in scope and emphasis, but the trend toward greater transparency is global: many jurisdictions are harmonizing accounting standards (such as convergence toward IFRS) and enhancing requirements around non-financial reporting, like environmental, social, and governance (ESG) metrics. Technological advances—real-time data systems, XBRL tagging, and automated compliance tools—are changing how companies prepare and publish filings, improving accessibility for stakeholders while raising new questions about data governance and cybersecurity in the reporting process.

Building and maintaining investor trust

Transparent earnings reports are a primary tool for building credibility with current and prospective investors. Regular releases demonstrate that the company is willing to be scrutinized and held accountable, which helps sustain long-term relationships with shareholders.

Reports typically include not only raw numbers but also management discussion and analysis (MD&A), which explains the drivers behind the numbers—such as changes in demand, cost pressures, or one-off events—and outlines strategic priorities. This context is crucial for investors trying to evaluate whether a company’s performance is cyclical, structural, or the result of temporary factors.

Guidance and expectation management

Many companies provide forward-looking guidance in their earnings releases or accompanying calls. Guidance narrows the gap between market expectations and company forecasts. When guidance aligns with or exceeds expectations, stock prices often respond positively; when guidance disappoints, the opposite can occur. Because of this dynamic, guidance is an important communication tool for managing investor sentiment and reducing market volatility around earnings events.

How earnings reports influence market prices

Earnings reports are high-salience events on a company’s calendar because they provide fresh information that markets incorporate into valuations. Analysts update earnings models and price targets based on reported results and management commentary, and traders quickly reprice shares to reflect the new information.

Volatility around earnings season is well-documented: positive surprises typically lift share prices, while negative surprises can trigger steep drops. This is why companies carefully time their releases and rehearse investor communications—to moderate reactions and ensure the message is clear and consistent.

Short-term reactions vs. long-term signals

Short-term stock moves can be dramatic but don’t always reflect a company’s long-term prospects. Investors focused on fundamentals will parse earnings reports for recurring trends—revenue growth sustainability, margin improvement, free cash flow generation, and balance sheet strength—rather than reacting solely to headline beats or misses.

Strategic communication beyond the numbers

Modern earnings reports combine quantifiable results with narrative. Management commentary often highlights strategic initiatives, capital allocation plans, market opportunities, and how the company intends to address risks. This narrative helps stakeholders understand the company’s trajectory and assesses strategic credibility.

Investor presentations, conference calls, and Q&A sessions provide opportunities for management to elaborate on the numbers and for analysts to probe assumptions. These interactions can clarify ambiguous items in the filings and reveal management’s priorities and competence in executing strategy.

Signaling and credibility

Consistent reporting and realistic guidance build credibility; inconsistent disclosures or frequent restatements erode trust. Investors watch not only for what is said but for what is omitted—failure to address key issues, such as rising costs or customer concentration, can be interpreted negatively and lead to reputational damage.

Wider effects: customers, suppliers, and partners

Earnings releases can influence more than just investors. Positive financial results and confident guidance can strengthen relationships with suppliers and partners by signaling stability and growth potential. Conversely, poor results may prompt suppliers to tighten payment terms or reduce credit exposure.

Research shows that consumers may also react to corporate earnings communications—visiting stores more often after favorable reports, for example—suggesting that earnings reports can function as a form of public relations and marketing in addition to financial disclosure. This consumer reaction demonstrates that earnings news sometimes reaches a broader audience than investors alone.

Practical purposes for management and internal stakeholders

Internally, preparing earnings reports forces management to analyze the business rigorously and document performance trends. The discipline of quarterly reporting drives better financial controls, forecasting, and alignment across business units.

Boards of directors, lenders, and employees use these reports to monitor business health and operational execution. Compensation plans and incentive structures are often tied to reported metrics, making earnings releases consequential for leadership accountability and workforce motivation.

Performance benchmarking

Quarterly and annual reports provide benchmarks against which to assess progress toward strategic goals. Whether aiming to increase market share, improve margins, or reduce leverage, the periodic nature of reporting allows stakeholders to measure momentum and course-correct if necessary.

Investor relations best practices

Effective investor relations (IR) goes beyond releasing raw numbers; it involves clear, consistent messaging and active engagement with the investor community. Well-run IR teams prepare detailed earnings decks, host webcasts, and provide timely follow-up information to ensure that market participants understand both the results and the strategic context.

Best practices include providing non-GAAP reconciliations, explaining one-time items, and offering as much forward-looking clarity as possible without crossing legal lines on forward-looking statements. Transparency over accounting policies and disclosure choices helps reduce confusion and builds credibility.

Risks, controversies, and the limits of earnings reports

While earnings reports provide essential information, they can also be manipulated or presented in a way that obscures the economic reality. Aggressive accounting, earnings management, or selective disclosure can paint an overly favorable picture. Regulators and auditors play a critical role in deterring and detecting such practices.

Investors should read beyond headlines and quarterly summaries to the footnotes and MD&A sections to understand assumptions and one-time factors. Independent analysis, including cash flow analysis and quality-of-earnings assessments, often reveals a clearer picture than headline earnings alone.

How to read an earnings report like a pro

Start with the income statement to see revenue and profitability trends, then check the balance sheet for leverage and liquidity, and review the cash flow statement for true cash generation. Focus on recurring operating performance and avoid over-weighting one-off gains or losses. Pay attention to margin trends, free cash flow, and changes in working capital.

Compare current results to prior periods and to analyst expectations, but also examine management’s explanations and any changes in guidance. Notes and disclosures often contain critical information about contingent liabilities, accounting policy changes, and significant related-party transactions.

Where to find reliable information

Primary sources are the company’s own filings and investor relations materials; regulatory filings with the SEC are authoritative and searchable. For context and expert analysis, reputable financial education sites and brokerage research can be useful. For an accessible primer on company earnings, practical guides like those from tastylive explain basic concepts, while organizations like FINRA offer investor-focused commentary on the impact of earnings season.

For academic insight into how earnings communicate with broader audiences, research from business schools highlights how consumers and other non-investor stakeholders can respond to corporate financial news. Industry resources such as Schwab’s investor education content also help explain what happens when companies report earnings.

Conclusion: earnings reports as a multifaceted tool

Earnings reports serve multiple essential functions: they fulfill regulatory obligations, provide transparency, and help build trust with the investment community. They influence market pricing, shape strategic narratives, and have ripple effects on customers, suppliers, and partners. Preparing for and interpreting these reports requires attention to both quantitative metrics and qualitative context.

For anyone interested in corporate finance—investors, analysts, employees, or customers—learning to read and evaluate earnings reports is a valuable skill. By combining careful numerical analysis with critical reading of management commentary and disclosures, stakeholders can better understand a company’s performance and prospects.

This content is for general information only and isn’t financial advice. Always do your own research and speak with a qualified advisor before making investment decisions. We can’t guarantee accuracy or outcomes, and you’re responsible for your own choices.

Article written by

Jared

Financial reports summarized by AI

No more 90-page PDF.