Reading time:

What is an earnings report?

Learn what an earnings report includes, how to analyze key financial statements, and how investors use these reports for insights into performance and strategy.

Article written by

Jared

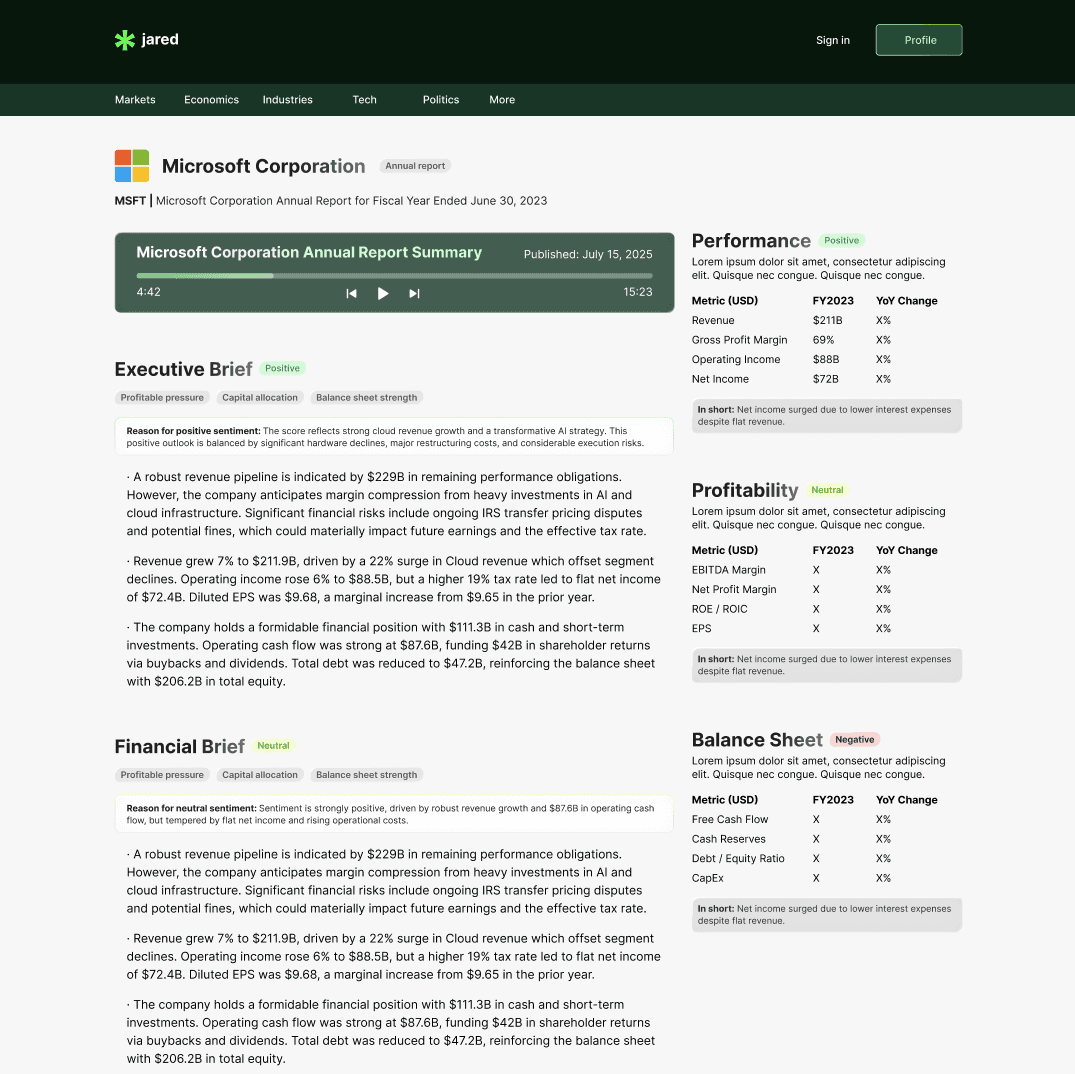

An earnings report is a document that public companies issue on a regular schedule—usually quarterly and annually—to disclose financial performance over a defined period. Investors, analysts, lenders and other stakeholders use these reports to evaluate profitability, cash generation, balance sheet strength and management's view of the business outlook. Because earnings reports combine numeric statements with managerial commentary and forward-looking signals, they play a central role in market pricing and corporate transparency.

Core components of an earnings report

At its core, an earnings report contains three standardized financial statements plus commentary that helps interpret the numbers. The income statement reports revenues and expenses; the balance sheet captures assets and liabilities at a point in time; and the cash flow statement explains how cash moved in operating, investing and financing activities.

Beyond these statements, earnings reports commonly include earnings per share (EPS) metrics, management's discussion and analysis (MD&A), notes to the financial statements, and sometimes non-GAAP performance measures that management believes highlight business trends. Each piece serves a specific purpose: numbers provide raw performance data, while MD&A and footnotes provide context and risk disclosures.

In addition, many earnings reports feature forward-looking guidance, where management offers estimates or expectations for future revenue, earnings, or capital expenditures. This guidance helps investors set expectations and evaluate the company’s strategic direction under current market conditions. Furthermore, earnings calls and investor presentations often accompany the report, giving stakeholders a chance to hear directly from executives about operational highlights, challenges faced during the quarter, and responses to analyst questions.

Supplementary disclosures might also include segment performance breakdowns, which reveal how different parts of the business contribute to overall results. For multinational firms, currency fluctuations, geopolitical risks, and regulatory changes are frequently discussed to explain variances from previous periods. These additional layers of detail enhance transparency and deepen investors’ understanding of the company’s financial health.

The income statement (profit and loss)

The income statement summarizes revenue earned and costs incurred during the period, producing a bottom-line net income (profit or loss). Key line items include total revenue or sales, gross profit, operating income, interest expense, taxes and net income. Gross and operating margins offer insight into pricing and cost control, while trends in revenue and operating expenses reveal whether growth is sustainable or margin pressure is emerging.

Seasonality effects and one-time items such as asset impairments, restructuring charges, or gains from asset sales are also typically highlighted on the income statement or within accompanying notes. These factors can distort the ongoing profitability picture, so analysts often adjust reported earnings to better estimate core operating performance. Comparisons with analyst consensus estimates and prior periods are integral to assessing whether the reported results meet, beat, or miss expectations.

The balance sheet

A balance sheet is a snapshot of financial position at the report date. It lists assets (cash, receivables, inventory, property), liabilities (debt, payables) and shareholders’ equity. Analysts often look at current assets versus current liabilities to assess liquidity, and debt levels relative to equity or earnings to judge solvency and financial flexibility.

Moreover, the composition and quality of assets are important; for example, a buildup in inventory might signal potential obsolescence or slowing sales, while increasing accounts receivable could indicate collection issues. On the liabilities side, short-term versus long-term obligations provide insight into the timing of upcoming cash demands. The balance sheet also reflects retained earnings and equity issuances or repurchases, shedding light on how profits are reinvested or returned to shareholders.

The cash flow statement

The cash flow statement reconciles net income to actual cash generated or used. It separates cash flows into operating (day-to-day business), investing (capital expenditures, acquisitions) and financing (debt and equity transactions). Positive operating cash flow is generally a healthier indicator than accounting profit, because it shows the business can turn sales into spendable cash.

When reviewing cash flows, analysts pay close attention to free cash flow — the cash remaining after capital expenditures — as it represents funds available for debt repayment, dividends, or expansion. Negative free cash flow might indicate heavy investment or operational issues. Additionally, changes in financing cash flows can reflect shifts in capital structure, such as issuing new debt, repurchasing shares, or paying dividends, all of which affect the company’s financial strategy and risk profile.

Key metrics investors focus on

Several concise metrics help translate complex financial statements into easy-to-compare signals. Earnings per share (EPS) indicates profit per outstanding share and is widely reported. Revenue growth communicates top-line momentum. Free cash flow measures cash after capital spending and provides insight into a company's ability to pay dividends, buy back shares or repay debt.

Margins—gross margin, operating margin and net margin—reveal how efficiently a company converts revenue into profit at different stages. Leverage ratios and liquidity ratios, such as debt-to-equity and current ratio, provide context on the balance sheet health. Trend analysis across these metrics is often more informative than a single-period snapshot.

Earnings per share (EPS) explained

EPS equals net income divided by the number of outstanding shares and can be presented as basic or diluted (which accounts for options, warrants and convertible securities). Market reactions often depend on whether reported EPS beats or misses analysts' consensus estimates, but a single beat or miss should be judged alongside revenue, margins and guidance to avoid overreaction.

Management’s Discussion and Analysis (MD&A) and other narrative sections

The MD&A is management’s opportunity to explain why results look the way they do and how the company views future prospects. It typically discusses drivers of revenue, cost trends, seasonality, market risks and strategic initiatives such as product launches, investments or restructuring. The MD&A helps translate raw numbers into a story about operational performance and strategic direction.

Footnotes to the financial statements are also essential. They disclose accounting policies, one-time items, contingencies and details that may materially affect interpretation—such as a large impairment charge, significant lease obligations or pending litigation. Non-GAAP measures are frequent in MD&A these can be useful but require scrutiny for consistency and reconciliation to GAAP or IFRS figures.

How to interpret an earnings report

Interpreting an earnings report requires a blend of quantitative comparison and contextual analysis. Start by comparing current results to guidance and to prior periods. Check whether revenue growth is organic or driven by acquisitions, whether margins are expanding or contracting, and whether cash flow supports reported earnings. Pay attention to recurring versus one-time items that might distort a single period's results.

Industry context matters. A company's weaker sales may be less concerning if the whole sector is slowing, while an outperformance in a weak market can signify competitive advantage. Compare results to peers' recent reports and to macro indicators—consumer spending, commodity prices or interest rates—that are relevant to the business model.

Comparative analysis and trend spotting

Quarter-to-quarter and year-over-year comparisons reveal trend direction. Seasonal businesses require year-over-year comparison for the same quarter to strip out cyclical effects. Longer-term trend analysis—over several quarters or years—helps identify structural changes in growth rates, cost patterns or capital intensity.

Red flags and positive signs

Red flags include consistently declining operating cash flow, rising receivables with stagnant revenue (which can signal collectability issues), increasing short-term debt, large and unexplained non-recurring charges, and persistent deviations between GAAP/IFRS results and management-adjusted measures without clear explanations. Positive signs include expanding margins, growing free cash flow, conservative guidance, and transparent disclosure in the MD&A and notes.

Recent regulatory change: IFRS 18 and its implications

Starting in 2027, IFRS 18 introduces new rules aimed at standardizing company-specific metrics and requiring enhanced auditability for performance measures outside of standard IFRS line items. The objective is to reduce the risk of misleading non-GAAP metrics and improve comparability between companies. Companies will need to provide clearer definitions and reconciliations for their bespoke performance measures.

This change will likely influence how management presents adjusted earnings, operational metrics and segment performance. Investors should anticipate more rigorous disclosures and potentially fewer ambiguous adjustments that previously obscured true operating performance. The broader effect should be improved transparency and easier peer comparisons for investors who rely on non-GAAP figures today.

Practical tips for investors and stakeholders

Before reacting to an earnings release, review the full package: press release, presentation slides, MD&A, financial statements and earnings call transcript. Watch for management tone during the earnings call and read analyst Q&A for clarifications. Focus on cash flow quality, sustainable revenue drivers and whether guidance is prudent or aggressive.

Use a checklist approach: verify revenue drivers, understand one-off items, evaluate cash flow and capital allocation, compare to peers, and note any changes in accounting policy. For long-term decisions, prioritize sustained free cash flow and competitive advantages over short-term EPS beats.

Reading between the lines of guidance

Guidance often signals management confidence and visibility into future demand. Conservative guidance followed by an upside beat can be positive, while consistently lowered guidance may indicate emerging challenges. Changes to guidance assumptions—like currency impact, commodity costs or anticipated product mix—are just as important as the headline numbers.

Common misconceptions and pitfalls

One misconception is that an EPS beat always equals a good investment. Short-term market reactions can be driven by small beats or misses, but the sustainability of earnings and quality of reporting matter more over time. Another pitfall is overreliance on non-GAAP measures without verifying reconciliation to standard accounting figures and understanding the adjustments.

Care should also be taken with seasonal companies and those undergoing structural changes—such as mergers or significant one-time charges—which can make a single quarter an unreliable signal. Instead, construct a multi-period view and consider the strategic context explained in the MD&A.

Conclusion: why earnings reports matter

Earnings reports provide a structured and regulated way for companies to communicate financial results and outlooks. They combine numeric statements with managerial explanation to form the basis for investment decisions, credit assessments and regulatory oversight. Proper interpretation requires attention to the core statements, key metrics like EPS and cash flow, and the qualitative context provided by management and footnotes.

With upcoming regulatory changes like IFRS 18, transparency around non-standard performance measures is set to improve, making it easier to compare disclosures across companies. For market participants, disciplined analysis—prioritizing cash generation, sustainability of earnings and clear disclosure—remains the most reliable path to informed decisions.

This content is for general information only and isn’t financial advice. Always do your own research and speak with a qualified advisor before making investment decisions. We can’t guarantee accuracy or outcomes, and you’re responsible for your own choices.

Article written by

Jared

Financial reports summarized by AI

No more 90-page PDF.