Reading time:

When do financial reports come out?

Discover how financial reports impact markets, when 10-Qs and 10-Ks are filed, and how investors use timing and earnings calls to guide decisions during reporting season.

Article written by

Jared

Financial reports are the backbone of market transparency. They reveal how companies performed, where revenue came from, what changed in expenses or cash flow, and what management expects next. Knowing when these reports arrive — and what to do when they do — helps investors, analysts, lenders, and other stakeholders make timely, informed decisions.

Types of financial reports and who must file them

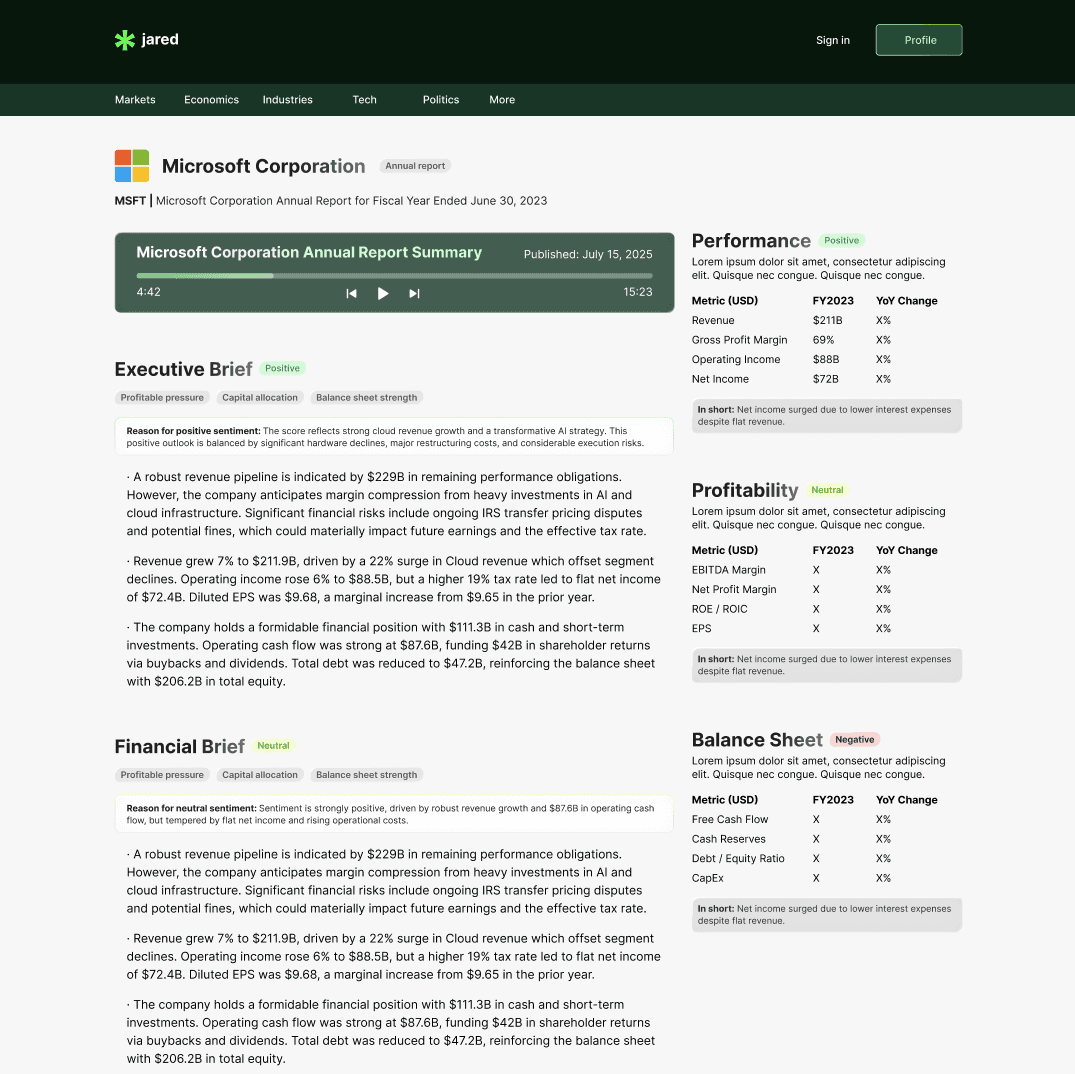

Public companies, particularly those listed in the United States, publish several types of financial filings on a regular schedule. The two most important recurring documents are quarterly reports and annual reports. Quarterly reports provide updates every three months, while annual reports offer a comprehensive review of the full fiscal year.

Regulatory obligations determine filing requirements. In the U.S., companies submit quarterly updates on Form 10-Q and annual reports on Form 10-K to the Securities and Exchange Commission (SEC). Smaller private companies and many foreign firms follow different disclosure practices, but public-company deadlines are the most relevant for market participants.

Beyond timing, these filings differ in content and depth: 10-Qs typically include condensed financial statements, interim management’s discussion and analysis (MD&A) of results, risk updates, and any material legal or operational developments since the last filing. The 10-K is much more comprehensive, containing audited financial statements, extensive footnotes, a fuller MD&A, a description of the business and risk factors, information about executive compensation, and disclosures about internal controls and corporate governance. Together these documents give investors and analysts the quantitative data and qualitative context needed to assess performance and prospects.

Other SEC filings are also important for market transparency. Companies must file Form 8-K to report significant events between periodic reports (such as mergers, changes in control, earnings releases, or departures of key executives), and proxy statements (DEF 14A) that disclose matters to be voted on by shareholders, including director nominations and detailed executive pay information. Filing deadlines vary with company size and classification—large accelerated filers face shorter deadlines than smaller reporting companies—and failure to file on time can trigger enforcement actions, trading suspensions, or investor litigation, while auditors and audit committees play key roles in ensuring the accuracy and completeness of the disclosures.

Quarterly reporting schedule: when the quarters close and when reports are due

Quarterly reports are filed after the close of each fiscal quarter. While many companies use the calendar year for their fiscal year, others use different fiscal year ends, so exact dates can vary by company. For calendar-year companies, quarter ends and approximate reporting windows usually align as follows:

- Q1 ends March 31; filings and earnings announcements commonly occur in April or May. - Q2 ends June 30; filings and earnings season typically plays out in July and August. - Q3 ends September 30; reports commonly appear in October or November. - Q4 ends December 31; companies report annual results in January through March, with the formal Form 10-K often filed within regulatory deadlines.

SEC filing deadlines for 2025 (example)

For public companies subject to standard SEC rules, Form 10-Q deadlines for fiscal year 2025 are set by regulation. The filing windows for that year are: Q1 — May 12, 2025; Q2 — August 14, 2025; Q3 — November 10, 2025; and Q4 — February 12, 2026. These dates reflect the maximum permitted filing times after the quarter end and can guide expectations for when reports and related earnings releases may appear.

Annual reports and the Form 10-K timeline

Annual reports synthesize a full year of financial performance, including audited financial statements, management’s discussion and analysis (MD&A), risk factors, and notes to the accounts. The Form 10-K is the formal SEC filing that contains these elements and is subject to deadlines based on company size and filer status.

For many calendar-year companies, the Form 10-K for the fiscal year ending December 31, 2025, would be due within 60 days after year-end for large accelerated filers in typical categories. Using the 60-day rule as a reference point, that deadline would fall on March 31, 2026. Smaller reporting companies and non-accelerated filers may have extended deadlines.

Earnings season: what it is and why it matters

Earnings season is the concentrated period shortly after a fiscal quarter ends when a large share of public companies release results. This clustering matters because it creates waves of market-moving information: analysts revise models, investors reposition portfolios, and media coverage intensifies.

For example, first-quarter earnings season in 2025 was expected to kick off in mid-May following the Q1 filing deadline. Major market participants monitor these broader windows closely, because correlated announcements across industries can influence macro narratives and sector rotation.

Typical cadence within an earnings season

Earnings seasons tend to follow a recognizable cadence. A subset of major companies — often banks, large tech firms, and retail leaders — report earlier in the season, setting the tone. Mid-cap and small-cap companies follow, and late reporters close out the season. Investors should expect volatility early as headline surprises are priced in, with more granular adjustments occurring as additional filings and conference calls provide detail.

Examples of scheduled reports and how they influence markets

Specific scheduled reports help anchor expectations. For instance, as of August 13, 2025, Alibaba Group reported results on that date, Walmart planned to report on August 21, 2025, and NVIDIA scheduled its report for August 27, 2025. Each of these companies operates in sectors closely watched by investors: e-commerce and cloud for Alibaba, retail and consumer trends for Walmart, and semiconductors and AI-related demand for NVIDIA.

When industry leaders report positive or negative surprises, their results often ripple through supply chains and peers. A strong quarter from NVIDIA, for example, can lift the entire semiconductor group as investors anticipate higher sales for suppliers and related software firms. Conversely, a disappointing retail print from Walmart could pressure discretionary stocks and signal consumer weakness.

Where to find financial reports and associated materials

Official filings are available through several reliable sources. The SEC’s EDGAR database provides free, searchable access to Forms 10-Q, 10-K, 8-K, and proxy statements. Companies also publish earnings releases, investor presentations, and archived conference call webcasts on their investor relations websites.

Beyond primary sources, financial news outlets, data providers, and brokerage platforms aggregate filing information and release calendars. Using multiple sources helps verify timing and fetch supplementary materials such as slides, guidance figures, and Q&A transcripts from earnings calls.

How to interpret timing and make it actionable

Timing matters for more than just knowing when to read reports. The decision to trade before or after an earnings announcement hinges on risk tolerance, investment horizon, and the information asymmetry between public filings and market expectations. Two practical approaches commonly used are:

- Event-driven analysis: Monitor companies scheduled to report and model expected outcomes based on consensus analyst estimates, prior trends, and guidance. This approach aims to capture moves around the announcement itself. - Long-term positioning: For investors with multi-year horizons, the quarter-to-quarter noise is less important than structural changes in revenue, margins, and cash generation. Quarterly results are useful checkpoints rather than trading signals.

Conference calls and guidance

Most companies hold an earnings conference call or webcast to discuss the results and answer analyst questions. These sessions often contain the most timely forward-looking information, such as management guidance and color on operational dynamics. Investors typically listen for changes in guidance, margin outlook, and any commentary on demand trends or supply-chain constraints.

Regulatory considerations and extensions

Filing deadlines are set by regulators, but companies can request extensions in limited circumstances. Late filings may trigger market scrutiny, stock-price reactions, or regulatory inquiries. Persistent delays have reputational consequences and may affect a firm’s access to capital.

Additionally, companies must report material events between periodic filings via Form 8-K. These can include mergers, leadership changes, or significant legal developments. Even though not part of quarterly or annual reports, 8-Ks can contain information that materially affects a company’s near-term prospects and should be monitored alongside scheduled reports.

Practical checklist for investors around report dates

To use financial reports effectively, consider a simple checklist that balances preparation and responsiveness:

- Mark filing and earnings dates on a calendar, including the anticipated earnings season windows for major indices. - Review consensus estimates and recent analyst notes to understand market expectations. - Read the earnings release and MD&A for key drivers and management commentary. - Listen to or read the transcript of the earnings call for questions that probe sustainability of performance. - Compare reported figures to consensus and the company’s prior guidance; focus on recurring metrics like revenue, operating income, and free cash flow. - Track any Form 8-Ks filed around the same time for unexpected material developments.

Common pitfalls to avoid

Several recurring mistakes diminish the usefulness of financial reports. First, reacting to headline earnings-per-share (EPS) figures without checking revenue trends or one-time items can lead to misinterpretation. Second, overemphasizing short-term volatility during earnings season risks misallocating capital if the investment thesis remains intact. Third, neglecting to adjust models for accounting changes or acquisitions may cause incorrect comparisons across periods.

Careful reading of footnotes, non-GAAP reconciliations, and the auditor’s opinion helps avoid these traps. Analysts and investors who dig beyond headline numbers tend to have a clearer view of long-term performance drivers.

Conclusion: timing is predictable, reaction is a skill

Financial reporting schedules are predictable: quarters close on set dates, regulatory deadlines define the maximum lag before filings must appear, and earnings seasons concentrate announcements. Using a structured approach to monitor filings, parse guidance, and interpret conference calls will produce better outcomes than reacting to surprises alone.

Knowing when reports come out is the first step. The next is developing a disciplined process to evaluate the content and link it to a broader investment thesis. With the right tools and habits, the regular rhythm of financial reporting becomes an advantage rather than a source of confusion.

This content is for general information only and isn’t financial advice. Always do your own research and speak with a qualified advisor before making investment decisions. We can’t guarantee accuracy or outcomes, and you’re responsible for your own choices.

Article written by

Jared

Financial reports summarized by AI

No more 90-page PDF.